The most top-of-mind electronics brand in the Netherlands isn't always the one people actually buy from. Behavio's Market Mapping study of the Dutch electronics category – six brands, twenty buyer needs, mapped from the consumer's side – found MediaMarkt owns the mind, bol owns the wallet, and Amazon.nl owns neither.

That gap, between the brand shoppers picture and the brand they buy, is the single most useful thing in the data.

Here's what the map showed, and what it means if you're trying to grow a brand in a category someone else got to first.

What did Behavio study, and how?

Behavio ran a Market Mapping study of the Dutch electronics category in June 2026. Market Mapping shows a category through the eyes of its buyers – it measures the fast, intuitive memory links between brands and needs, the associations that actually drive choice.

The study covered 648 category buyers (people who buy electronics at least once a year), drawn from a representative national sample of 1,500 Dutch adults, balanced by age, gender, geography, and socio-economic status. Six brands were mapped: bol, MediaMarkt, Coolblue, Amazon.nl, Expert, and Megekko.

For each brand, the study measured four things: how much each of twenty needs matters to buyers, how strongly each brand is linked to each need, the same links adjusted for brand size (we call this the Differentiation View), and brand health – awareness, salience, buyers, and likeability.

Why does the market split by heritage, not channel?

Almost every brand in electronics now sells online and in stores. So the old online-versus-offline line no longer explains anything. What still explains a lot is where each brand was born.

Brands born online (bol, Amazon.nl, Megekko) are strongly associated with price, choice, and convenience. Brands born in stores (MediaMarkt, Expert) are more tied to advice, service, and the big, considered purchases. Heritage didn't fade when everyone got a website. If anything, it hardened.

Coolblue is the exception that proves the rule. It started online, then deliberately built stores, hired its own installers, and grew a service reputation. Today, it owns store-type strengths (installation, expert advice) despite its online roots; proof that heritage is a strong influence, not a fixed sentence.

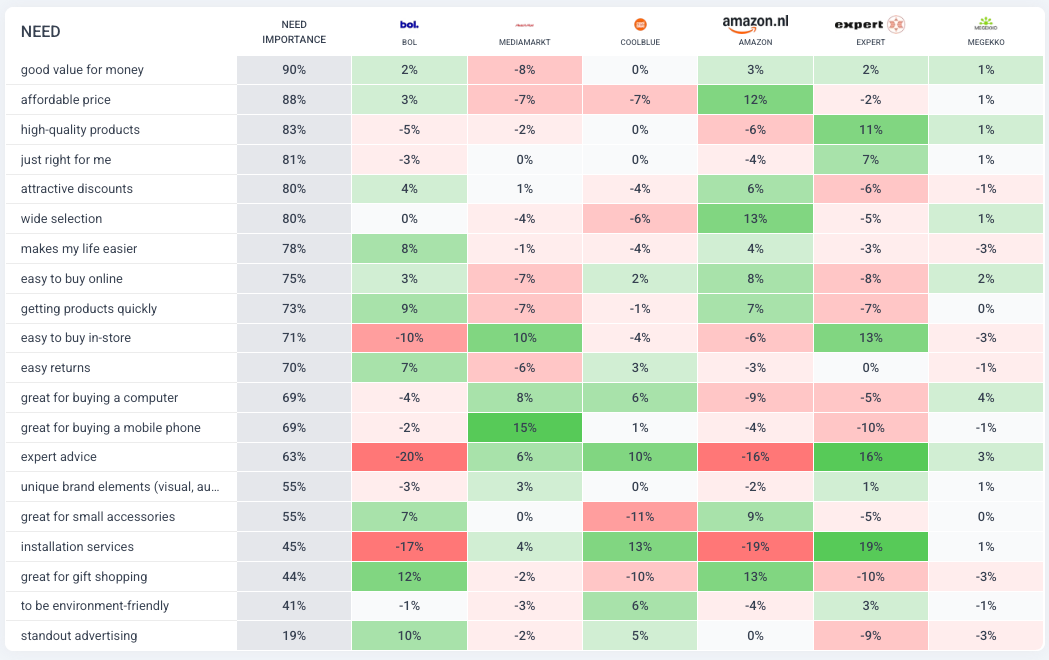

Group the twenty needs into four buckets – price and quality, convenience, advice and service, purchase size – and each one tells a cleaner version of the same story.

1. Price skews to the marketplaces, quality to the stores

Good value, affordable price, high-quality products, and discounts are the needs buyers care about most. In the Differentiation View, they split cleanly. Amazon over-indexes hardest on affordable price (+11). Expert is the clear differentiator on high-quality products (+6). Discounts skew to Amazon (+6) and bol (+4), away from Expert (−7).

But on good value for money – the single most important need in the whole market – every brand sits within ±2 of expected. Nobody differentiates. The need everyone wants is the need nobody owns.

"Cheap" is an online trait, "good" is a store trait, and "value" is still up for grabs.

2. Convenience is online territory, full stop

Amazon over-indexes hardest on wide selection (+12) and easy to buy online (+11). bol punches above its weight on making life easier (+8) and getting products quickly (+7).

MediaMarkt and Expert run negative on every convenience need. This is marketplace ground, and store heritage can't cheaply buy it back.

3. For advice and installation, shoppers still want a store

The widest gaps in the whole study show up here. On expert advice, Expert (+16) and Coolblue (+12) tower above expectations, while bol (−19) and Amazon (−14) collapse. Installation services repeats it: Expert (+17), Coolblue (+13), versus −17 for both marketplaces.

The more a need depends on a human helping you, the more it belongs to the brands that grew up with humans in stores.

The one exception is easy returns, where bol is the only brand that over-indexes (+8). For a pure online player, returns is a logistics problem, not a service counter. It’s solved with process, not people.

4. The bigger the purchase, the more the store wins

Split the category by how much the decision matters, and the pattern is clean. Considered, expensive buys tilt to the stores: MediaMarkt over-indexes on mobile phones (+11) and computers (+8).

Quick, low-stakes buys tilt online: bol leads gift shopping (+12) and small accessories (+6), with Amazon strongly positive on both. Tellingly, store-shaped Coolblue goes negative on exactly these throwaway buys.

Marketplaces win the small stuff. Stores win what people are afraid to get wrong.

Why does MediaMarkt own the mind but bol own the wallet?

This is the finding worth sitting with. Three brands ended up in three completely different places.

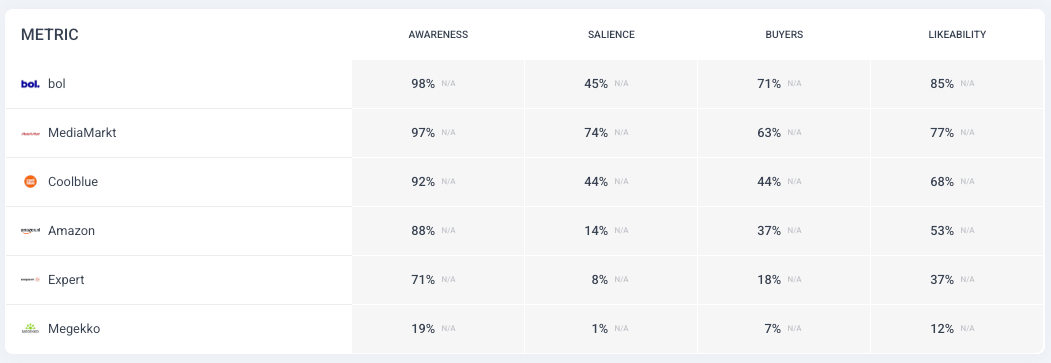

MediaMarkt owns the mind. It has the highest electronics salience by far (74% versus bol's 45%) and near-total awareness (97%). Shoppers picture the store, and it owns the considered purchases.

bol owns the wallet and the heart. It has the most buyers (71%) and the warmest feeling in the market (85% likeability). But its salience sits mid-pack at 45%. People use bol and like bol – they just don't picture it first when it comes to buying electronics.

Amazon.nl owns neither. It's known by almost everyone (88% awareness) but bought by only 37%, and it leads in none of the twenty needs. Its salience is just 14%. Awareness was never Amazon's problem. Getting picked is.

Why the split? MediaMarkt's store heritage makes it the brand shoppers picture for electronics. But most purchases are quick and price-led, so the click goes to bol. The pictured store only wins the transaction when the basket is big enough to be worth the trip. Salience sets the shortlist; convenience closes the sale.

The market data agrees with the map. The Netherlands is one of only two Western European countries where Amazon isn't the leader. It still trails bol on sales – roughly €1 billion to bol's €3.1 billion in 2024 – despite committing over €1.4 billion to the market through 2027.

Only one brand converts fame into category recall

Line awareness up against salience and the pattern is stark. Only MediaMarkt turns fame into electronics recall (97% aware, 74% salient). The generalists leak it: bol by 53 points, Amazon by 74. The specialist gets remembered for electronics. The generalists get remembered for everything, which means for nothing in particular.

Being pictured is not the same as being bought. In the electronics market, distribution beats memory, right up until the purchase gets big enough to send the shopper back to a store.

What does this mean for your brand?

The same map reads differently depending on where your brand was born. The move is never to chase every need at once. It's to own the one your history already earned you.

If you're store-born: Your edge is advice, service, and the purchases people fear getting wrong. A marketplace can't copy that with a faster warehouse. Defend it, don't burn budget out-pricing bol on cables.

If you're online-born: You win the wallet, not the category mind. Closing the salience gap – being pictured, not just used – is your growth lever. And if you own no distinctive need at all, pick one and start building.

As Behavio CEO and brand expert Jiri Boudal puts it: "The mistake is chasing every need at once. Find the need your brand already half-owns, the one your history earned you, and own it completely. That's where growth is cheapest and stickiest."

Want this map for your category?

This is what Behavio's Market Mapping shows: who owns which need, where you punch above your weight, and the one thing your brand is already half-known for. Run it for your market and stop guessing which need to fight for.

- Who Owns the Dutch Electronics Market? – Behavio Market Mapping study, June 2026 (n=648 Dutch category buyers, from a nationally representative sample of 1,500 adults)

- Amazon Invests €1.4 Billion in the Netherlands – Cross-Border Magazine, 27 Oct 2025

- Amazon Goes 'BOL'd' With €1.4B Investment in the Netherlands – Silicon Canals (citing ECDB), 27 Oct 2025

Frequently asked questions

It depends what you mean by "leader." MediaMarkt leads on salience; it's the brand most Dutch shoppers picture first for electronics (74%). But bol leads on actual purchase, with the most buyers (71%) and the highest sales, roughly €3.1 billion versus Amazon's ~€1 billion in 2024. The Netherlands is one of only two Western European markets where Amazon isn't the leader.

Market Mapping is a research method that shows a category through the eyes of its buyers. It measures the fast, intuitive memory links between brands and consumer needs (the associations that actually drive choice) rather than what people say in a survey.