.avif)

The Dutch outdoor retail market looks simple on the surface. People need gear, clothing, and equipment to explore nature, hike, cycle, or travel.

But when you look at what shoppers actually expect from outdoor retailers, the picture becomes much more nuanced.

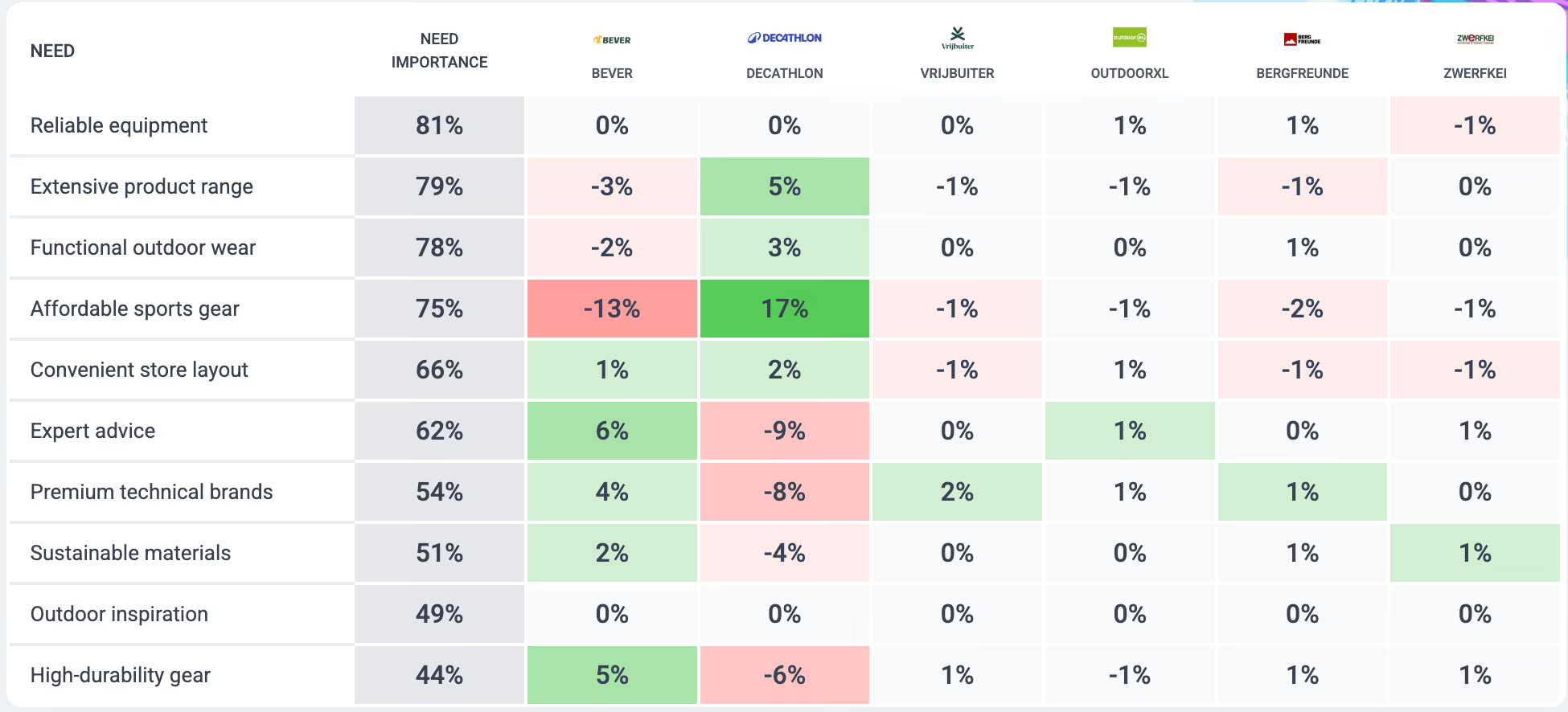

Using Behavio’s market mapping data, we analyzed how Dutch category buyers associate key outdoor needs with major retailers: Bever, Decathlon, Vrijbuiter, OutdoorXL, Bergfreunde, and Zwerfkei.

By comparing two things —

- how important each need is to shoppers

- which brands people associate with those needs

— we can see not only who dominates the category today, but also which brands stand out in consumers’ minds.

And one thing becomes immediately clear: most brands compete on the same fundamentals, but only a few manage to differentiate.

The fundamentals of outdoor retail: reliability and range

Before looking at individual brands, it’s important to understand what matters most in this category.

For Dutch outdoor shoppers, the top priorities are highly practical:

- Reliable equipment — 81%

- Extensive product range — 79%

- Functional outdoor wear — 78%

- Affordable sports gear — 75%

These are the table stakes of outdoor retail. Any brand that wants to compete must perform well here.

Further down the list, but still important, are elements like:

- Convenient store layout (66%)

- Expert advice (62%)

- Premium technical brands (54%)

- Sustainable materials (51%)

Interestingly, emotional or lifestyle-oriented needs rank lower, with outdoor inspiration (49%) and high-durability gear (44%) sitting at the bottom.

This tells us something fundamental about the category: performance and practicality dominate consumer expectations.

But meeting these expectations doesn’t automatically create differentiation.

Bever: the premium outdoor specialist

Bever stands out as one of the strongest brands across the category’s key needs. It scores high on several of the most important associations:

- Reliable equipment: 72%

- Extensive product range: 72%

- Functional outdoor wear: 71%

- Expert advice: 71%

- Outdoor inspiration: 72%

This broad strength reflects Bever’s long-standing position as the dedicated outdoor specialist in the Netherlands.

When we adjust for brand size to examine relative differentiation, Bever’s clearest strengths appear in:

- Expert advice (+6%)

- High-durability gear (+5%)

- Premium technical brands (+4%)

These are signals of a brand perceived as knowledgeable and technically credible. However, Bever shows a significant weakness in one important category driver:

Affordable sports gear: –13%

In other words, consumers see Bever as expert and premium, but not the place for value. This creates a clear positioning: Bever wins on expertise and credibility, not on price.

Decathlon: the category giant of accessibility

Decathlon performs exceptionally strongly on the category’s functional needs. It leads the market on several key associations:

- Extensive product range: 78%

- Functional outdoor wear: 73%

- Affordable sports gear: 75%

- Reliable equipment: 69%

These numbers reflect Decathlon’s global positioning: broad range, functional performance, and affordability.

But what’s even more striking is Decathlon’s relative differentiation. Compared with competitors, it dominates one of the most important needs in the category:

Affordable sports gear: +17%

No other brand comes close. This confirms Decathlon’s strongest mental territory: accessible outdoor gear for everyone.

The brand also performs positively on:

- Extensive product range (+5%)

- Functional outdoor wear (+3%)

However, Decathlon underperforms in areas linked to expertise and premium positioning:

- Expert advice (–9%)

- Premium technical brands (–8%)

This makes strategic sense. Decathlon isn’t trying to be the specialist gear authority. Instead, it wins by being the most accessible and affordable gateway into outdoor sports.

Vrijbuiter: the mid-tier generalist

Vrijbuiter sits somewhere between the large-scale retailers and the smaller specialists.

Across most needs, its absolute associations fall around 25–31%, far below category leaders.

For example:

- Extensive product range: 31%

- Functional outdoor wear: 30%

- Reliable equipment: 30%

In the relative comparison, its scores hover close to zero. That means consumers don’t strongly differentiate Vrijbuiter from competitors.

It occupies a middle position in the category: visible, present, but not strongly defined by any particular need.

This kind of position can be risky. Without a clearly owned mental territory, brands can easily become replaceable in consumers’ minds.

OutdoorXL, Bergfreunde, and Zwerfkei: low mental availability

The remaining brands in the dataset share a similar challenge.

Across almost all needs, associations remain very low, typically 8–13%. Their differentiation scores are also minimal, rarely exceeding +1% or –1%.

This doesn’t necessarily mean these brands are weak businesses. But it does suggest that their mental availability among Dutch outdoor shoppers is limited.

In other words, many consumers simply don’t think of them first when outdoor needs arise.

This is a classic brand growth challenge. Without strong mental associations, even good retailers struggle to compete with larger, more established players.

What the outdoor category reveals about brand competition

When you step back from individual brands, a clear pattern emerges in the Dutch outdoor market.

1. Functional strength dominates the category

Most of the highest-importance needs relate to performance and practicality:

- reliable equipment

- product range

- functionality

- price

These are category fundamentals, not differentiators.

2. Price and expertise define the competitive divide

Two brands clearly own opposite ends of the market:

Decathlon → affordability and accessibility

Bever → expertise and premium credibility

This split reflects two different shopper mindsets:

- entry-level outdoor enthusiasts looking for value

- experienced adventurers looking for specialist advice

3. Many brands still lack a clear mental territory

Several retailers in the market show low associations across all needs. That suggests the outdoor category still has open mental territory.

Future growth may come from brands that successfully claim areas like:

- sustainability leadership

- adventure inspiration

- community and outdoor lifestyle

These dimensions matter less today, but they could become powerful differentiators over time.

The bigger picture: owning a moment in the outdoor journey

The Dutch outdoor market shows a familiar pattern seen in many retail categories.

Everyone competes on the same functional benefits. But consumers only remember a few brands for them.

And that’s the key lesson.

In competitive retail categories, success rarely comes from offering the same benefits as everyone else. It comes from owning a specific role in the customer’s journey — the moment when people decide where to go.

Behavio’s market mapping shows that these mental territories are constantly evolving. The brands that manage to secure one of them early are the ones that shape the future of the category.

Frequently asked questions

Decathlon and Bever stand out most clearly. Decathlon dominates affordability and accessibility, while Bever is strongly associated with expertise, premium gear, and specialist outdoor knowledge.

Dutch outdoor shoppers prioritize highly functional needs. The most important drivers are reliable equipment (81%), a wide product range (79%), functional outdoor wear (78%), and affordable sports gear (75%).

- Bever Market Tracking – Behavio, January 2026